Questions about the dollar and inflation and gold continue to rise. Let’s follow the money and address the same.

35 shares

A Bit of Bull

As the new year kicks in, a number of diverse yet qualified opinions and pundits are back in full swing ringing the warning bells for the future of the US dollar and inflation and the fate of our markets.

In other words, is it all about to come crashing down? Should you run for the hills?

The short answer is “no.” The longer answer is “not yet.”

Below we explain why there’s still a bit of fight left in this bull run as we take a deeper dive into the dollar and inflation, the markets and the ultimate value of gold.

The U.S. Dollar and Inflation—A History of Relative Rather than Actual Strength

As for the U.S. Dollar and inflation, its story, like just about every story related to the securities market, the Main Street economy, the global currency exchange (FX market) or the destiny of precious metals essentially (and not surprisingly) boils down to one thing: The Fed

We all remember the emergency measures taken by Bernanke’s Fed when the sub-prime mortgage crisis reared its hitherto ignored head and sent Wall Street and most of its broken banks to their knees in 2008.

The solution? Trillions of dollars were printed and interest rates were sent to zero.

In fact, so many dollars (over 3.5 trillion of them) were printed, that the world expected massive inflation and a tanking dollar. By 2010, the dollar had found a floor and gold had hit new highs as it was universally believed the dollar was in free-fall. This dollar and inflation rise, however, didn’t play out as expected.

The Rest of the World Loved a Cheap Dollar

In this setting of low rates and a falling dollar, the rest of the world saw what they believed was a bargain. Countries and companies across the globe, from the Emerging Markets and Latin America to China and the Middle East, were all thinking the same thing: Borrow more dollars!

After all, rates in the US were cheaper than in their own local currencies. Furthermore, with the Fed printing all that money, these foreign borrowers just assumed the diluted U.S. Dollar had nowhere to go but down, and hence would be easier to repay. That was their expectation regarding the dollar AND inflation.

And so, gobs and gobs of foreign sovereigns and CFO’s took out 30-year adjustable-rate mortgages in dollar denominated debt and naturally assumed that when the day came to settle these debts, it would be painless, as the inflated dollar would be even weaker (and hence easier) to pay back. That was the consensus view as to the dollar and inflation.

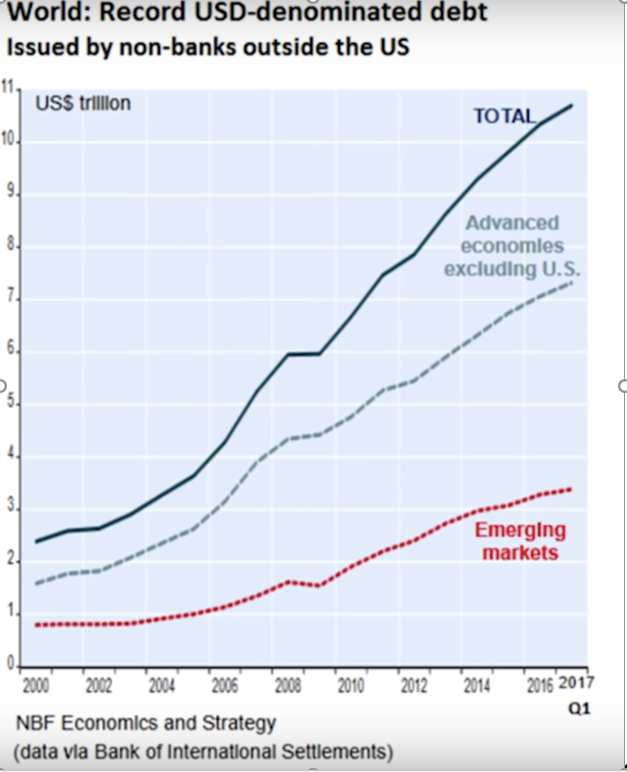

And so the debt binge denominated in U.S. Dollars took off!

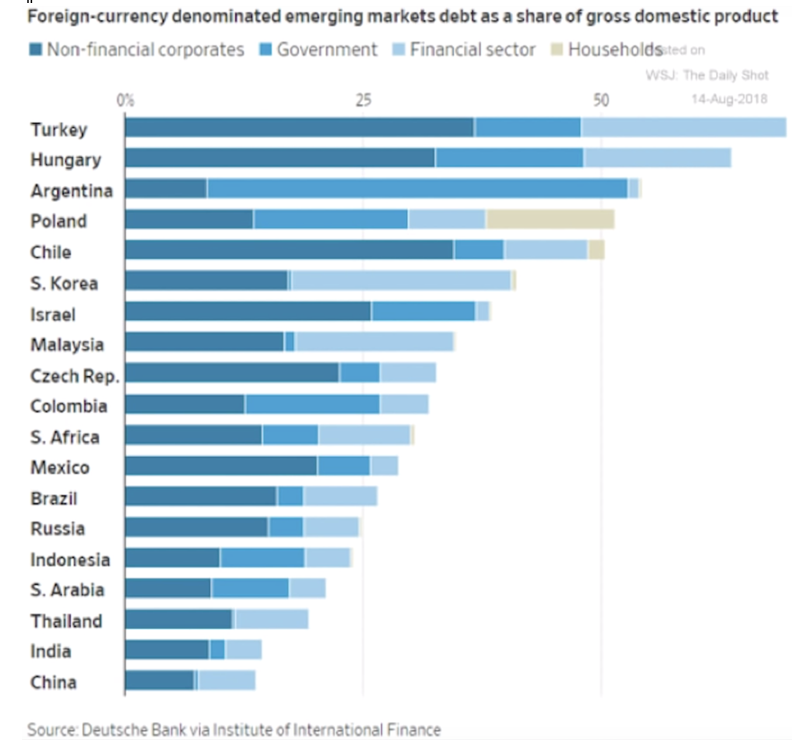

Between 2008 and 2015, countries like Turkey, Hungary and Argentina went on a massive U.S. Dollar borrowing binge, which explains why outstanding dollar-denominated debt in those zip codes now exceeds 50% of their GDP (!).

And they weren’t alone with this dollar and inflation gamble. Effectively the whole world was thinking the same thing and hence borrowing the same dollars at incredibly high levels, as the graph below confirms:

But with all these countries and foreign companies doing the same thing at the same time, they unintentionally created their own nightmare.

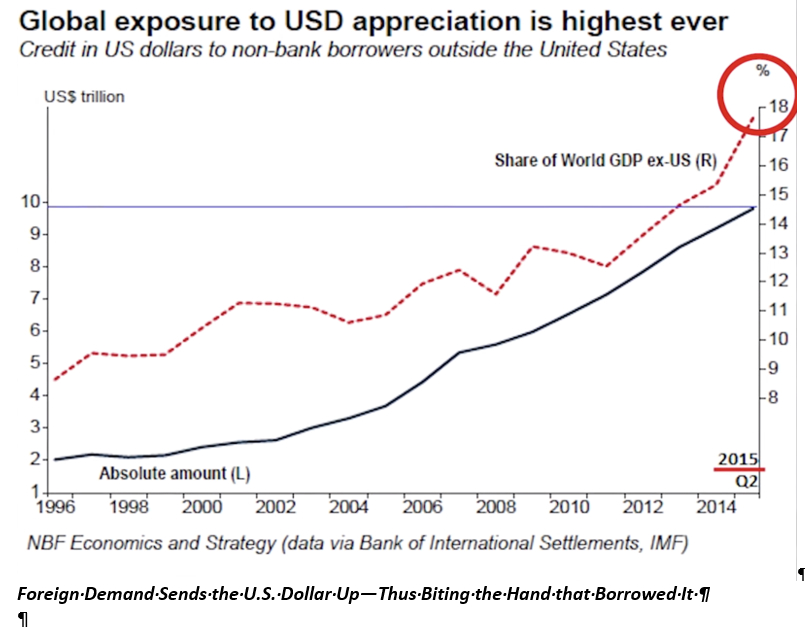

That is, as widespread and simultaneous demand for the dollar hit the moon, the dollar got stronger, not weaker. The old belief about the dollar and inflation was coming undone.

This further meant that repayment of those debts got harder, not easier. The pain and cost of this dollar-appreciated debt to foreign debtors has now reached record highs, which amount to 18% of global GDP..

In order to borrow these once cheap US Dollars, foreign institutions and governments were thus selling their own local currencies to buy the Greenbacks necessary to repay the interest and principal on their original loans.

In this collective backdrop of global borrowing, demand for the US Dollar sky rocketed even more. This demand further eroded the dollar and inflation theory, as the dollar got stronger, not weaker.

And as we learned in high school econ, when demand for something rises, so too does its price and value, which meant the US dollar rose in value relative to other currencies like the Peso, Yen and Euro.

Even More Dollar Demand from Foreign Investors

Meanwhile, in Europe and Japan, bond yields had fallen below zero in the backdrop of an insane monetary policy running at full speed overseas. Pure madness.

Needless to say, if you’re a Japanese or European institution or pension fund looking for yield, where else could you go but the U.S.?

At 2%-3% (depending on the year), even anemic US yields were a heck of a lot better than anything foreign investors could find in their own markets.

Net result? More flows of foreign investment into U.S. markets and U.S. dollars, and thus once again the old dollar and inflation theory fell even more, as the dollar strengthened rather than “inflated” away.

This meant even more demand for US stocks and bonds from the big investors overseas, which meant more and more of foreign players were dumping their Yen and Euros and buying US dollars, which meant more demand for US dollars, and hence a rising valuation for US dollars.

A rising US Dollar may seem like a good sign, but in central bank distorted backdrops like the post-08 new abnormal, a strong dollar actually does more damage than good.

First, a strong dollar makes it exceptionally hard for US companies to compete in the international export market, as the cost of US widgets is higher and thus less competitive overseas, which helps explain the horrifying decline in US export hegemony since 2000, a topic we recently addressed directly.

A Rising Dollar and Inflation?

Despite earlier and current disconnects between the dollar and inflation, as demand for the US Dollar increases, this can eventually cause a scenario where we see a rising dollar AND inflation occurring at the same time, something most econ students, Fed chairmen and pundits now say never happens.

But in a new abnormal in which central banks have so thoroughly changed the current rules of market action, anything can happen.

We are now seeing an over-supply of US Dollars occurring on two fronts: A) the Fed is printing again, with its balance-sheet now over $4 trillion and B) foreign inflows of US dollars are at massive levels to both pay back dollar-denominated debt or capture the last crumbs of yield in. our markets.

Such inflows of dollars can lead to unwanted inflation, the kind the Fed can neither “target” or control. With inflation comes rising rates, and rising rates are to a debt bubble what shark fins are to a surfer—bad news.

Of course, we are taught that inflation only occurs when the dollar is diluted and weakening, but in the post-2008 central bank-driven Twilight Zone, we now face a scenario where the dollar can rise in strength at the same time rates and inflation are also rising. In short, the relationship between the dollar and inflation is complex.

The simultaneous fact that we are seeing shortages of dollars in the Euro Dollar markets is a counter-force to this dollar and inflation morass.

Strange things happen in strange times, and as we argued—and later saw—in 2019, one can also see scenarios where the dollar rises alongside a rising gold price, a correlation hitherto thought implausible.

A Vicious Circle

This potential for more inflation and hence rising rates means even higher debt payments for foreign entities with dollar-denominated debt—all of which is on adjustable (rather than fixed) interest-rate repayment schedules.

In other words, those countries borrowing US dollars will have to print even more and more of their local currencies in order to pay back a rising (rather than falling) US Dollar, which was the very opposite of their original plan.

In other words: Oops.

This explains why countries like Argentina and Turkey are seeing fatal inflation at home with their Peso and Lira tanking in value, as they have had to print (and dilute) their local currencies at such astronomical levels just to buy enough dollars to meet their U.S. Dollar-denominated debts—debts they originally thought would be based on a falling rather than rising dollar.

This creates a vicious circle of increasingly broke countries having to print more money to meet U.S. debt obligations, and hence more and more demand for US Dollars, thereby making future debt obligations increasingly harder to repay. This tug-of-war between inflation fears and a rising US dollar based on dollar demand is never-ending, but for now is keeping dollar inflation at bay.

Which means foreign debtors from Argentina to Turkey are increasingly beginning to resemble the sub-prime mortgages of 2008, that is: Massive in size and equally massive in their risk of collapse.

More Tailwinds for Now

In the near-term, however, the foreign demand for US Dollars and securities is enjoying its last hurrah and hence we predict more dollar strength ahead, and more market highs before the fall.

The great irony, however, is that at some point the dollar demand makes that same dollar too strong to repay, and then we can anticipate defaults on dollar-based loans and a subsequent crisis in dollar-based markets, one so large that a second Plaza Accord could be needed to deliberately weaken the dollar, as was done in 1984-85.

But not yet.

For now we see a clear scenario where despite inevitable pockets of stock volatility, the dollar inflows from overseas into the relatively higher-yielding corporate and government bonds in the US will be a tailwind not only for US bonds, but stocks as well, thus adding to melt-up in the securities markets we saw and signaled in 2019.

Printing Dollars for Foreign Markets?

Unfortunately, however, the debt and inflation levels overseas are getting so crazy that at some point the US Fed will more than likely be forced to print trillions more dollars in the coming years which it can then give to foreign players to help them repay their debts to us–an otherwise classic case of circular fraud masquerading as stimulus.

More Dollars, More Flows, More New Market Highs Ahead

Either way, such additional money creation will slowly add to inflation levels as well boost near-term inflows into US markets—all of which bodes as a major near-term boost for US stocks and bonds. See how complex the game between the dollar and inflation can get?

In short, we bemused market realists (and long-term bears) nevertheless foresee a clear bull-case scenario for now, one in which the dollar will strengthen, inflation (not the bogus kind “reported” by the US CPI) will climb and the US markets will rise, thus setting the stage for a continued melt-up in 2020, failing any further repo risks, massive rate cuts or black swans out of Asia.

But Keep Your Eyes Forever on Managing Risk

As always, however, and given the immense degree of distortion, risk and uncertainty today, one must temper such enthusiasm.

As the dollar (and dollar bubble) rises due to its status as the best horse in the global glue factory, we nevertheless must and will face an inevitable day of reckoning when the dollar’s inflationary winds and over-valuation turn ironically against itself, for the day can and will come when the dollar becomes too strong to be sustainably repaid by oversees borrowers.

At that point, the dollar will come crashing down rather than sky-rocketing up.

Although likely years rather months down the road, the dollar’s hegemonic days, including its status as the world’s reserve currency, are numbered, as England’s own Mark Carney has all but prophesized.

Furthermore, as inflation creeps up, interest rates will follow and eventually reach a level fatal to U.S. credit markets—a genuine end-game moment that we are always tracking.

In the near term, however, the current rise in the US Dollar’s strength (and US stocks) should continue to trend up, which means the money printing from other central banks necessary to pay for these dollars and stocks should continue as well.

Golden Setting

Such continued money printing, outside and inside the U.S., will only make gold all the more valuable when the entire can-kicking charade of printing from the left hand to pay the debts of the right hand can no longer sustain itself, for remember: debt can’t be rolled over forever.

This means our stance on gold as flood insurance in the backdrop of a world drowning in fiat currencies remains unchanged.

For now, however, expect bumpier yet continued market highs ahead. We see more and more foreign inflows and hence more and more tailwinds, not only for the Greenback, but for U.S. securities in general.

That said, we must concede that there are others—including smart billionaire bond jockeys like Jeffrey Gundlach—who are less optimistic. They see the US dollar’s (and US market’s) rise ending much sooner.

For now, and regardless of whether the U.S. Dollar and market’s current rise is long or short-lived, the end result is still the same: markets will correct, and hence the cash recommendations of our Storm Tracker should remain forever in place and a part of your current plan.

Comments

5 responses to “The Dollar, Markets, Inflation, and Gold: Just Follow the Money”

- John says:

Hi

Is the cash recommendation in Stormtracker still at 30%. And can you tell me how I can access more info on Stormtracker please? Thanks

Rgds

John

- Scott says:

“With inflation comes rising rates, and rising rates are to debt bubble what shark fins are to a surfer-bad news.”

Given that the Fed has a pretty massive balance sheet of crap, isn’t it possible that inflation could be contained with unwinding of balance sheet assets by the US Fed? This would seem more practical than jacking rates in my opinion.

- Wood Robsays:

Beautiful….Just Beautiful…. thank you for the superior

Modern update of true modern economics! Should our portfolio possibly now include a lager percentage of equites poised to rise with a trailing stop to sell at some level then have some ability to automatically buy a different investment with a higher likelihood of rising as the rest of the markets fall?

- Bob McGovernsays:

I’m reading the Creature from Jekyll Island and sometimes I feel like I’m reading a book of fiction. I can’t believe how long these practices have been going on. I read and just shake my head. Is there any hope that common sense will prevail? Thanks for all the great information that you guys are putting out. I devour your emails when they come in. I will be following your direction like a hawk. Keep it up!

- Brian O’Donnellsays:

Wow, such a neat article to read. So informative and easy to understand. Wel done authors. Well done indeed. Brian